Real estate investing comes with plenty of moving parts, but at the heart of it all is one big question: How much money is this property really making me? Gross yield provides the first answer to that question. But what is gross yield, and how does it work? It’s one of the simplest yet most powerful metrics investors use to judge whether a rental is worth the price tag.

In this article, we’ll break down what gross yield means in plain language, why it matters when you’re sizing up a deal, and how you can calculate it for smarter investment decisions.

Main Takeaways

-

Gross yield is the “headline number” in real estate investing, showing rental income compared to property price before expenses.

-

It helps investors screen deals, compare properties, and set expectations, but it should be weighed alongside net yield and cap rate.

-

Practical tools and strategies make tracking easier, and expert management ensures those numbers translate into real returns.

What Is Gross Yield?

What Is Gross Yield?

What Is Gross Yield?

What Is Gross Yield?When it comes to making reasonable profits, Baltimore property management is all about staying on top of the numbers. One of the key measures we rely on is gross yield — it gives us a quick snapshot of how an investment is performing. With it, investors get a fast way to see if a property is performing well compared to its purchase price.

So, what exactly is gross yield? In real estate terms, gross yield is the amount an investment property brings in before you subtract expenses like taxes, maintenance, or insurance. Think of it as the “headline number” — the raw return you’d expect just from rental income compared to the property’s purchase price.

Tools to Calculate and Track Gross Yield

To gain a better understanding, let’s look at how to calculate and track gross yield. This way, you’ll know exactly how to go about it and which tools can make the process easier.

Helpful Tools to Track Gross Yield

While you can use a simple calculator or spreadsheet, many investors prefer software that keeps everything organized:

Stessa

Stessa is a free tool for property management and accounting. You can hook up your bank accounts or simply upload your numbers, and it does the tracking for you. Rent, expenses, even property values — it keeps it all in one place. You get reports in just a few clicks, and it shows you key metrics like gross yield in real time.

BiggerPockets Rental Property Calculator

This is one of the most popular tools for analyzing quick deals. All you need to do is enter the property price, expected rent, and estimated expenses, and it runs the numbers for you. Investors like it because you can easily compare multiple properties side by side and see which one offers the stronger gross yield or cash flow potential.

Buildium

Buildium is a more advanced, full-service property management platform. First, it helps with yield calculations, lets landlords manage leases, track rent payments, screen tenants, and create detailed financial reports.

Gross Yield Formula:

Gross Yield (%) = (Annual Rental Income ÷ Property Purchase Price) × 100

Example:

Say you bought a rental property for $250,000, and it generates $24,000 in rent each year.

Gross Yield = (24,000 ÷ 250,000) × 100 = 9.6%

That 9.6% is your gross yield, that is, a quick snapshot before expenses are factored in.

How Gross Yield Affects Investment Decisions

How Gross Yield Affects Investment Decisions

How Gross Yield Affects Investment Decisions

How Gross Yield Affects Investment DecisionsWhen you’re looking at a property, gross yield gives you the first gut check on whether it’s worth considering. It’s quick math, but it instantly shows you how much income the property is generating compared to what you’re paying for it. Investors use this number to quickly screen deals, especially when comparing multiple options.

That said, experienced investors know gross yield isn’t the whole story. A property might look great on paper with a high yield, but if it’s in a risky neighborhood or comes with high maintenance costs, those returns can shrink quickly. This is why many landlords view gross yield as the starting point; it is a way to determine if a deal warrants a closer look.

Another way gross yield impacts decisions is in setting expectations. For instance, a 5% yield in a high-demand city may be more valuable in the long term than a 10% yield in an area with weak rental demand. Investors weigh these numbers against their goals — some want steady cash flow right away, while others prioritize long-term appreciation.

Ultimately, gross yield can inform financing and management decisions. Lenders often look at potential rental returns when approving loans, and property managers rely on yield figures to set competitive rents. Understanding how gross yield ties into the bigger picture helps investors make smarter moves, from picking the right property to choosing the right strategy.

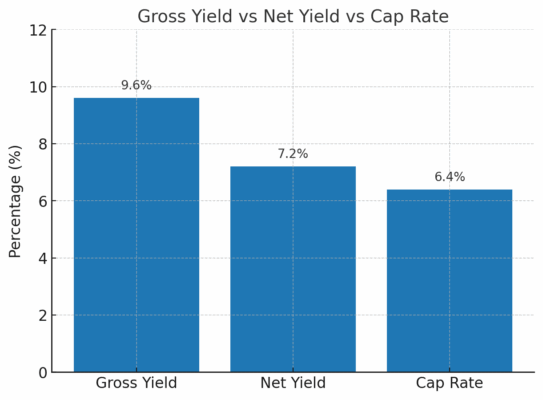

Gross Yield vs Net Yield vs Cap Rate

For you to really see the profit from a rental, you can’t stop at gross yield. That’s just the first step. You also need to check net yield and also look into your cap rate. Each one tells the story a bit differently.

Let’s look at the formulas:

- Gross Yield = (Annual Rent ÷ Purchase Price) × 100

- Net Yield = (Annual Rent – Expenses ÷ Purchase Price) × 100

- Cap Rate = (Net Operating Income ÷ Market Value) × 100

Metric |

What It Means |

Formula |

What It Tells You |

| Gross Yield | Income before expenses | (Annual Rent ÷ Purchase Price) × 100 | Quick snapshot of return potential |

| Net Yield | Income after expenses | ((Annual Rent – Expenses) ÷ Purchase Price) × 100 | More realistic view of actual profits |

| Cap Rate | Return based on property’s current value | (Net Operating Income ÷ Market Value) × 100 | Useful for comparing properties in the same market |

Example:

- Say you buy a rental for $250,000 and it generates $24,000 a year in rent. That works out to about a 9.6% gross yield.

- Now, take out yearly expenses — let’s say $6,000 — and the net yield comes down to roughly 7.2%.

- And if the property’s market value goes up to $280,000, then the cap rate shifts to around 6.4%

As you can see, gross yield gives you the fastest “first look,” but net yield and cap rate bring you closer to the real performance of the investment. Experienced investors check all three before making a decision.

When Should You Use Gross Yield?

When Should You Use Gross Yield?

When Should You Use Gross Yield?

When Should You Use Gross Yield?Gross yield is most useful at the very start of your investment search. It tells you if a property is worth looking into before you get into all the detailed numbers.

For example, if you’re comparing three rentals side by side, gross yield provides an easy way to identify which one appears stronger on the surface. It’s also handy when you’re scanning listings or running early deal analysis, because the math is straightforward and doesn’t require a lot of extra data.

That said, experienced investors treat gross yield as the first step, not the final answer. Once a property passes the gross yield test, that’s when you move into deeper metrics like net yield, cap rate, and cash flow to see if the deal really makes sense long term.

Turning Gross Yield Insights Into Real Returns

Gross yield may seem like a simple calculation, but it plays a big role in guiding investment decisions. From comparing properties quickly to spotting portfolio trends, it gives investors that first snapshot of a property’s potential.

At Bay Property Management Group, we help investors put these numbers into action. Our services are designed to maximize returns and keep your rentals performing at their best, including:

- Setting competitive rental rates to keep your property attractive and profitable

- Tenant screening and placement to reduce risk and minimize vacancies

- Full rent collection and accounting so your income and expenses are tracked with ease

- Maintenance coordination that keeps costs in check and properties well cared for

- Regular financial reporting so you always know how your investments are performing